2026-27 Budget

Adopted Budget Book Approved Budget Book Proposed Budget Book

Questions from the Budget Committee

View a PDF of the questions and answers

Fund 100 Questions

1. Page 15, Resources Function 1990 Miscellaneous Revenue: What accounts for the relatively large increase in budgeted miscellaneous revenue in the general fund? $800,000 is a big increase over the $300,000 budgeted in FY25-26 and the $171,591 actually received in FY24-25.

The district receives various donations, reimbursements, stipends, and other payments which are recorded as miscellaneous revenue. In addition, when we need to correct a prior year transaction, such as an invoice received after the fiscal year has closed, a credit for an expense in a prior year, or any correction after the fiscal year, this correction is recorded to “Prior Year Recovery.” That account is shown as a revenue account, but it can be a positive or negative balance, just depending on the type of correction. As we continue to clear prior-recorded invoices from our pending liabilities, or write off items, we record these items here. There are several aging accounts payable that we expect to write off, which will result in this account increasing.

2. Page 15, Resources, Function 1915 Building Lease Payments: there is $0 proposed. HOLLA leases one of our buildings. Do they pay rent? Also, where does the funding for land used by McMenamins for parking go?

HOLLA is leasing what was the Four Corners building. The rent is included as part of their Charter School agreement. McMenamins leases the parking lot during concert season (May to October). This revenue will be donated to the Reynolds Education Foundation to help fund mini-grants for schools. In the 200 Fund, local revenue has been added for $20,630.50. This is offset by an expense in function 3390 for 400 Supplies, which will be the cost of mini grants. Multnomah ESD leases two of the Edgefield buildings and we have confirmed that they will continue leasing through June 2027. Revenue for this has been added to the proposed budget ($120,000).

3. Page 15, Resources Function 2101 Intermediate Sources: Why is the County School Fund going down? Also, what is the County School Fund?

The County School Fund is a distribution from Multnomah County based on revenues received from property taxes associated with railroad cars and the sale of timber cut on federal forest land. This is a statutory responsibility of Oregon counties (ORS 308.505 to ORS 308.665). The County School Fund revenue is deducted from our State School Fund payment, so the net resources to the district is neutral.

4. Page 15, Resources, Function 3102 State Sources: What is the revenue hold for SSF? What are the conditions needed to secure these funds? What happens if we DON’T secure these particular funds?

Expenditures exceed estimated revenue by $1,050,000 at the time of the budget proposal release. This line item is to allow for spending authority as we anticipate additional revenue from a combination of SSF adjustments, ending fund balance, and the final 2024-25 enrollment reconciliation. If we do not realize the additional revenue, or if estimated expenditures increase, then additional reductions will be necessary.

5. Page 16, Resources, Function 5000 Other Sources: The beginning fund balance is listed as $4m but isn’t our current ending fund balance closer to $2m?

Yes. We expect that we will not spend all currently encumbered funds (e.g. on a purchase order to be expended or reserved for a vacant position). This would be a reduction in current year expenditures and therefore increase the ending fund balance.

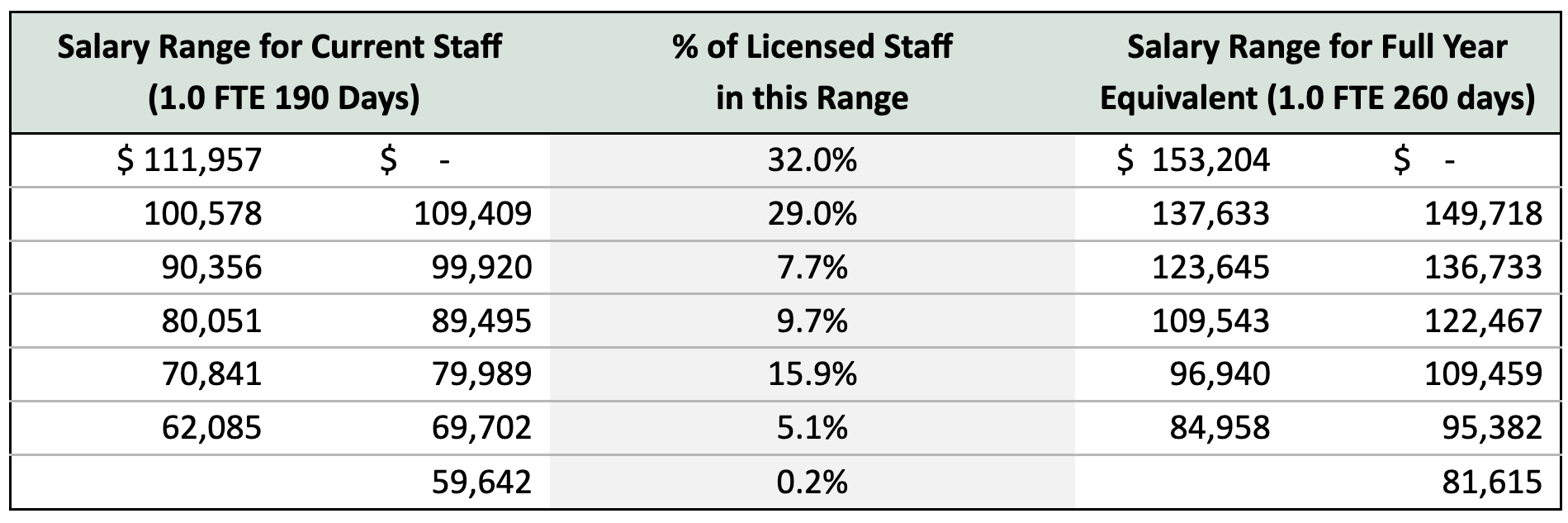

6. Page 16, Object 111 Licensed Salaries: What is the average salary for an RSD teacher?

The average salary for a licensed staff member is $97,710 for 1.0 FTE 190 days; the 260-day equivalent is $133,709

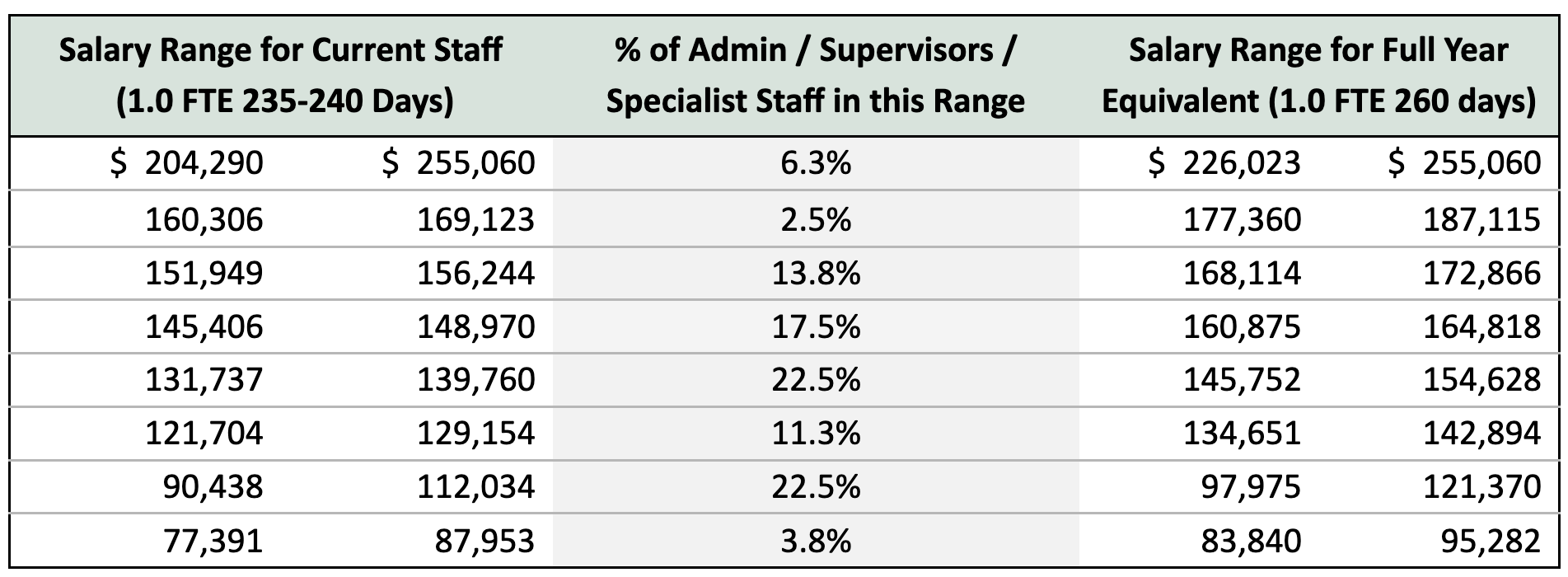

7. Page 16, Object 113 Administrators Salaries: What is the average salary for an RSD administrator?

The average salary for administrators/directors is $147,544 for 1.0 FTE 235 days; the 260-day equivalent is $162,780. The average salary for supervisors/specialists is $96,896 for 1.0 FTE 240 days; the 260-day equivalent is $104,971.

8. Page 16, Object 112 Classified Salaries: What is the average salary for a classified employee?

The average salary for classified staff is $38,988 for 6.72hrs daily at 202 days; the 260-day equivalent at 1.0 FTE is $57,857. 92% of classified employees work four or more hours per day and earn on average $41,270 (or $58,883 for the 260-day equivalent at 8 hours). 33% are full time (8 hours) and earn $61,847 for the 260-day equivalent period.

9. Page 17, Function 1111 Elementary Programs, 300 Purchased Services: What does the amount of approx $1.2 million entail?

$993,638 licensed substitutes, $207,538 classified substitutes, $25,000 30-day EAs, and $1500 rentals/leases.

10. Page 17, Function 1132 High School Athletics, 100 Salaries Regular: It looks like two FTE are getting paid approx $316k each. Can you explain?

100 Salaries Regular includes more than just pay for specific FTE: $141,092 is for salary costs for the 2.0 FTE for the athletic trainer and secretary; $43,490 is for additional hours to pay classified staff who support athletic activities; $449,314 is for coaching stipends.

11. Page 18, Function 1220 Restrictive Programs, 300 Purchased Services: Why is there an increase of $775K?

This increase is similar to prior years and is primarily related to annual increases for contracted services through MESD for Behavioral Health, Support, and Helensview.

12. Page 18, Function 1225 Out of District Programs: What is this function for? Is this something we are legally obligated to provide?

1225 Out of District Programs includes Early Childhood Intervention services through David Douglas SD ($860,000) and Columbia Regional Inclusive Services for the Deaf and Hard of Hearing programs ($730,000). Open School and Rosemary Anderson programs have been restricted to currently enrolled students.

13. Page 19, Function 1229 Other Special Programs, 300 Purchased Services: This line item is more than double the previous year. What is this for?

1229 Other Special Programs includes contracted services through MESD for functional life skills programs at Wheatley School and substitutes for RSD staff in the Community Transition Program. These program costs vary based on the number of placements in each program each year.

14. Page 19, Function 1250 Less Restrictive Programs, 300 Purchased Services: This line item is more than double the previous year. What is this for?

The increase reflects the cost of substitutes for staff in this function.

15. Page 19, Function 1288 Charter School: Is there a specific revenue for the charter schools or does it come from the general State School Fund for the district?

Charter schools are paid from the general fund. The District receives ADM for students in charter schools based on the state school fund allocation. Each month the district receives a state school fund payment, we pay each of the charter schools based on the rate determined by the charter school agreement. ODE mandates the charter school ADM per student, then the district pays based on the pass-through rate agreed upon in the charter contract.

16. Page 19, Function 1288 Charter School: Can we subtract the cost of these teachers from their pass through money?

Generally, charter schools employ their own staff. RSD is responsible for providing special education FAPE. A small number of RSD special education staff are assigned to charter schools. They are not reflected in this function.

17. Page 20, Function 1299 Other Programs: This requirement is nearly double the previous year and includes 3 additional FTE. What is this for?

This reflects licensed salaries for dual language immersion programs, which are expanding annually.

18. Page 20, Function 1299 Other Programs: Who are these 8 FTE?

Licensed teachers for dual language immersion programs.

19. Page 20, Function 2110 Attendance / Social Work: There is $23,680 proposed for regular salaries and $8,288 for associated payroll costs but there are 0 FTE. What is this funding?

This funding is for additional hours on timesheets for SPED tutoring programs.

20. Page 20, Function 2115 Student Safety: We reduced FTE by approx 10. Are these primarily SMTs?

Reduction of 7.48 FTE Campus Monitors; Reduction of 2.78 FTE ISS Monitor Note: updated budget moves 0.75 FTE for Health and Safety Asst to function 2410

21. Page 20, Function 2115 Student Safety: Does this category include school resources deputies?

Yes. $319,856 is budgeted to continue the contract with the Multnomah County Sheriff's Office.

22. Page 20, Function 2120 Guidance Services: We reduced counselors by six FTE. Where are we losing these positions?

The 6 FTE reduction was a shift of funding sources to grants. The actual reduction in staff is 2 FTE (.5 Glenfair/.5 Margaret Scott, 1.0 RHS). Every elementary school will still have a full time licensed counselor. No reductions at middle schools or RLA. RHS was reduced from 8 to 7 counselors.

23. Page 21, Function 2150 Speech Pathology and Audiology Services: I don’t understand how we’re reducing this requirement by two FTE yet only saving approx $600.

The cost of salaries increases, even if the FTE does not change, due to step and COLAs. Additionally, other costs increased primarily related to substitute/temporary staff to cover absences and vacancies.

24. Page 21, Function 2190 Services Direction Support Services: We’re reducing this requirement by nearly half the FTE. What is this for and what will we lose?

The total reduction is 5.17 FTE for TOSA positions from the General Fund. Two of these FTE will remain and be shifted to available grant funds.

25. Page 21, Function 2190 Services Direction Support Services: What type of services are under this category?

Medicaid billing and claiming fees, contracted staffing services for vacancies and leaves of absence, legal fees, and conference fees for required training.

26. Page 21, Function 2190 Services Direction Support Services: There is $795,597 proposed for 6 FTE, which is approximately $130,000 each. What positions are these?

1 Director for Student Services; 3 Program Administrators; 1 Bookkeeper; 1 Secretary; Additional hours for SPED IEP meetings

27. Page 21, Function 2210 Improvement of Instructional Services: We’re increasing this requirement by approx $190K. What will this be used for?

This year we have expended over $150k on licensed substitutes as of March; the budget reflects the estimated total cost of the full year.

28. Page 22, Function 2230 Assessment and Testing: How are we increasing FTE but decreasing salaries?

The 25-26 budget included .5 FTE for the Director of Assessment and Systems Improvement position and 1 FTE for a classified testing coordinator position. There are now 2 FTE classified testing coordinator positions funded here and no administrators.

29. Page 22, Function 2241 Instructional Technology: There is $0 allocated for FTE. Do we not have teachers for media, technology, or computer science? Do those classes exist at Reynolds?

In 2024 the salaries coded to this function included the Director of Technology and 2.0 FTE for Instructional Technology TOSAs. TOSA positions were eliminated. The director position in FY24-25 was coded to Function 2660 Technology Services and then moved to 2661 for FY25-26 and FY26-27. Licensed media specialists are in Function 2220 Educational Media Services. Licensed technology electives are in Function 1121 for two middle schools. Licensed CTE computer FTE is in Function 1131 for RHS.

30. Page 22, Function 2241 Instructional technology: We’re increasing this function by $345K. What will this be used for?

For the next budget year, replacement and replenishment of 9th grade devices are coded to this function, as well as the software licenses for Google Chrome OS management. In some years, there are grant funds to offset the replenishment cycle. In addition the cost for FY25-26 was paid for in June FY25-26.

31. Page 22, Function 2310 Board of Education, 300 Purchase Services: What does the $190,000 proposed include?

This includes professional services for our bond consultant ($40,000), our annual audit ($85,000), legal services ($30,000), and election services ($35,000).

32. Page 22, Function 2310 Board of Education, 600 Other Objects: What does the $14,000 proposed include?

Other objects includes dues and fees for our annual OSBA membership and subscriptions ($12,000), and our annual payment to the Oregon Ethics Commission ($2000)

33. Page 23, Function 2410 Office of the Principal Services: What are the positions funded under this requirement for?

7.00 FTE Assistant Principals; 1.00 FTE HS Bookkeeper; 0.06 FTE Crossing Guard; 1.00 FTE Dean of Students; 8.82 FTE Health & Safety Assistant (this will increase by 0.75 FTE moving from 2115); 10.95 FTE Noon Assistant; 16.00 FTE Principal; 1.00 FTE RHS Receptionist; 2.00 FTE HS Registrars; 20.70 FTE Asst Secretary; 1.00 FTE Attendance Secretary; 16.00 FTE Lead Secretary

34. Page 23, Function 2490 Other Support Services - School Administration: There is $85,951 proposed for 0.50 FTE. What position is this? And how does this position support Academic Success, Safe & Well-Maintained Facilities or Student Safety, Support & Wellness?

This is the Director for Federal Programs position, which is split funded between general fund and federal/state grants with a strong focus on Title I-A, II-A, IV-A, Student Investment Account, High School Success, Early Literacy which all provide funding and support for student academic success, and health and safety.

35. Page 23, Function 2510 Direction of Business Support Services: There is $211,380 allocated for 1.00 FTE. What position is this? Last year's budget had $221,593 for 2.50 FTE. How are we reducing FTE from 2.5 to 1.0 but only reducing salaries by $10K?

Function 2510 Director of Business Support Services is the Managing Officer position. This position was in function 2520 in FY25-26 and updated to function 2510 starting this year. In prior years, the district receptionist positions and the executive assistant for operations were coded to this function. The reception positions are now in function 2630 Communications and the executive assistant position is now in function 2541 Service Area Direction Facilities.

36. Page 23, Function 2510, Direction of Business Support Services, 600 Other Objects: What are we funding for under this line item?

This is a portion of the liability insurance.

37. Page 23, Function 2520 Fiscal Services, 100 Salaries: FTE went from 11 to 0 under this requirement. Are these positions now in the following functions: 2521, 2523, 2524, 2525? Am I correct in understanding we now have 8 FTE in the finance department from the previous 11 FTE?

Correct, the Financial Services team is now moved to specific functions related to their roles. Adopted FTE was 11.0 FTE, one position was closed. In 25-26, budgeted FTE is 10.0, but 2.0 FTE were left vacant this year; the budget for 26-27 is for 10 FTE.

38. Page 23, Function 2523 Receiving and Disbursing Funds Services: There is $77,018 allocation for 1.00 FTE. This category was $0 for the last three years. How did we do it with no funding those years?

This is for a specialist position in the Finance department; previous to this year, there were 2.0 FTE for this position, listed in function 2520.

39. Page 24, Function 2544 Maintenance Services, 300 Purchased Services: What are the increases in this line item for? What will it be used for?

There is not an increase but rather a change in location. 2542 Custodial Services was reduced by $1.6 million and $1.3 million was added to 2544 Maintenance Services. This change better reflects the nature of the services, such as elevator monthly maintenance service, HVAC repairs, fencing, refinishing gym floors, playground equipment repairs, boiler services, glass replacement, and similar services.

40. Page 25, Function 2545 Building Fixed Costs: What kinds of items are in this function?

This function is where our utility and monthly service costs are recorded for water, electricity, natural gas, water and sewage, garbage, alarms and security monitoring, telephone, and postage.

41. Page 25, Function 2550 Student Transportation Services: If salaries are being moved to Function 2552 Vehicle Operation Services, why is there still funding allocated to salaries and payroll with no FTE?

2550 is the “umbrella” function for the underlying functions. Most of the additional hours, which are the payroll costs listed in 2550, are for bus drivers in 2552 and for routes specific to students eligible for special education in 2558.

42. Page 25, Function 2558 Transportation - Special Education, 100 Salaries: If we are reducing FTE by 1.28, why is the amount for salaries increasing?

Classified staff receive a 4% step and 2% COLA this year. We reduced FTE costs by around $45k, but the remaining 28 positions (18.60 FTE) cost an additional 6% which is around $1,900 for each position. This is an example of how, even if we were to keep the exact same FTE (‘roll up’), the cost would increase due to step, COLA, taxes, and other payroll costs. To keep the same number of staff (or FTE), the rate of payroll cost increase would need to be less than the additional revenue or we would need to reduce other costs.

43. Page 26, Function 2572 Purchasing Services and Function 2573 Warehousing and Distribution Services: What are the differences between these two categories? The 1.00 FTE in 2572 earns almost double what the position in 2573 earns. Please explain.

The 2572 Purchasing Services function is Financial Services. The position funded from this function is the procurement and contracts specialist. The 2573 Warehouse and Distribution function is Facilities. The position funded from this function is for the district courier classified position.

44. Page 26, Function 2573 Warehousing and Distribution Services, 100 Salaries: It looks like we are keeping a 1.0 FTE but paying them less than the previous year?

It is not the same employee; the position is paid the same salary scale but on a different step than the previous employee.

45. Page 26, Function 2630 Communications: I thought we cut the Director of Communications. What other positions are in this function? What positions are we adding to Communications?

There are no new positions being added to the Communications department. This function includes 1.0 FTE for the Language Services Supervisor (same as last year) and 1.50 FTE for the district receptionists (moved from function 2510).

46. Page 26, Function 2640 Staff Services, 100 Salaries and 200 Associated Payroll Costs: If there are no FTE, why are there salaries and payroll costs?

Stipend costs for professional development are coded here.

47. Page 26, Function 2641 Undesignated: $213,414 allocated for 1.00 FTE. What position is this?

This function is for HR Service Direction (we have corrected from “Undesignated”). The FTE is for the Managing HR Officer which was previously coded to 2640 Staff Services, the “umbrella” function for this group.

48. Page 27, Function 2649 Other Staff Services: There is $114,191 allocated for 1.00 FTE. What position is this?

$80,000 is for the admin assistant to the HR and Finance teams. The other $34,000 is to pay staff for building moves per the licensed contract.

49. Page 27, Function 2649 Other Staff Services, 200 Associated Payroll Costs: Why is the associated payroll costs so much larger than the salary?

This function is where the REA insurance pool contribution is budgeted ($350,000), under object 243 for insurance.

50. Page 29, Function 7000 Unappropriated Ending Fund Balance: Is this ending fund balance less than 5% of the general fund?

No. $8,070,910 is the rounded amount of 5% of budgeted revenues ($161,418,134 x .05 = $8,070,907)

Note: Board Policy requires 5% of Revenue to be reserved for ending fund balance. In Public Budgeting, Revenue is money collected or received in the current year, while Resources are other types of funding available, such as beginning fund balance or transfers. To calculate Total Revenue, it is the sum of funding sources in the 1000, 2000, 3000, and 4000 revenue codes.

Fund 200

51. Page 31, Resources, Function 1920 Donations: There is $400,000 proposed. Where will these donations come from? And where will they be allocated?

These revenue funds are for Fund 261 School-held donations and grants, and Fund 262 Reynolds Education Foundation donations and grants. Typical donations are from grantors such as Meyer Memorial Trust, Lemelson Foundation, Nike, Kroger, Blackbaud Giving, and various independent donations. The allocation depends on the specific donor requirements, and spending only occurs if there is a confirmed donation.

52. Page 31, Resources, Function 1990 Miscellaneous Revenue: There is $1,374,999 proposed. Where do these funds come from and where will they be allocated?

This provides sufficient authority for receiving payments related to these programs:

$100,000 Drivers Education

$150,000 E-Rate Program

$350,000 Energy Efficient Schools program

$100,000 Miscellaneous grants and donations held by the district

$500,000 Student Activity fees and fundraising

$525,000 Insurance claims and reimbursements

Allocations for expenditures depend on the source and program; only actual revenue received will be approved for spending.

53. Page 31, Resources, 5000 Other Sources: There’s a beginning fund balance of $7.2m, which is different from the Fund 100 balance. Why is there this much here?

Ten sub-funds within the 200 Special Revenue fund are expected to have carry forward funds, which are specific to each of those programs. Fund 200 is a collection of specific revenues and resources that are restricted to specific purposes.

- 238 Youth Transition Program. We are reimbursed at a specific rate, not at the actual cost of services. About $30,000 is expected to be available to offset program costs that are not included in the reimbursement rate.

- 252 E-Rate program. We received funds in a prior year. $580,000 is expected to carry forward.

- 253 Energy Efficient Schools. Senate Bill 1149 requires that Oregon's two largest investor-owned utilities, Portland General Electric (PGE) and PacifiCorp, collect a 1.5% "public purpose charge" from customers. Public K-12 schools within the PGE and PacifiCorp service areas receive 20% to implement energy efficiency projects and/or purchase zero emissions vehicles or electric vehicle chargers within the school districts. While the district receives these funds monthly, it is considered an advance to the district - no expenditures may occur until a project is approved by the program administrators (State of Oregon). The district is holding approximately $3.6 million in funds that may be used to support upcoming replacements and renovations to HVAC systems. Note that the nature of these types of projects require saving and holding this revenue until funds are sufficient to support the proposed project.

- 257 Contract Fuel Sales. The district provides fuel to other government agencies and bills for the cost plus administrative fees. This is approximately $100,000.

- 260 Student Activity Fund. Funds held by schools but not yet expended are carried forward to the following year; these funds may only be used for the purpose cited when raised.

- 261 Non ASB Grants and Fees. The budget is holding $200,000 for carryforward of grant and donation funds still in progress.

- 270 MYC Fee for Services. RLA coordinates the Multnomah Youth Corp program which collects and raises funds throughout the year to support the summer program. $60,000 is budgeted for this purpose.

- 297 Nutrition Services. Nutrition Services is expected to break even or better. The current end of year balance is approximately $100,000.

- 298 Early Retirement. Early Retirement provides the funding to pay for contractually obligated stipends and health insurance for retiring employees, who may retire at any point during the year. Funds budgeted but not used carry forward to the following year and may reduce the general fund transfer. $80,000 is expected to carry forward.

- 299 Insurance Reserve. Insurance reserve funds are for deductibles, settlements, and other emergency needs under various insurance and legal claims. Funds budgeted for the insurance reserve but not used carry forward to the following year and may reduce the general fund transfer. $1,700,000 is expected to carry forward.

54. Page 33, Function 1131 High School Programs, 100 Salaries: If we are reducing FTE by 1.0, why is the amount of salaries increasing?

Increases in staff costs (step/longevity/COLA/stipends) mean that the same FTE costs more.

55. Page 34, Function 1133 High School Activities, 400 Supplies and Materials: What are we purchasing in this line item?

This is for Fund 260 Student Activities and is for supplies related to student clubs and activities.

56. Page 35, Function 1272 Title IA/D, 300 Purchased Services: We are increasing this line item by nearly $300K. What are we purchasing?

Approximately $105k is for substitutes for staff positions in this fund; Approximately $184k is for Charter School payments required under Title I programs for students enrolled in schools outside of the district.

57. Page 35, Function 1280 Alternative Education, 100 Salaries: How are we reducing FTE by only 0.5 and reducing salaries by over $100K?

The FY25-26 budget supports one licensed FTE, related costs and stipends paid to students for the MYC summer program. The proposed budget is for a halftime classified position.

58. Page 36, Function 1400 Summer School Programs: Since we didn’t receive funding from ODE for summer school, are we eliminating these costs?

We propose to keep the budget authority both to run essential programs and in the hopeful chance that funds are provided in a supplemental grant award. Expenditures will not occur in this fund unless revenue is confirmed.

59. Page 36, Function 2122 Positive Behavior Supports/Restorative Justice, 400 Supplies and Materials: What are we increasing this line by $176K for?

Title I is $43,352 of the total and Comprehensive Support and Improvement/Targeted Support and Improvement (CSI/TSI) funds are the balance. We have been correcting functions within grants to better reflect the grant requirements and the actual reason for purchases.

60. Page 37, Function 2210 Improvement of Instructional Services: How are reducing FTE to 0 but still have salaries and payroll costs?

Additional time sheet hours for data teams are billed to this function.

61. Page 38, Function 2240 Instructional Staff Development, 300 Purchased Services: What are we increasing this line item by nearly $185K for?

Much of this budget is for the Title IIA grant and is related to professional development. $126,545 has been recorded here for professional development to improve instruction such as MANDT training and ECRI training. Additionally, $60,900 is budgeted for related substitute costs for staff to attend training would also be coded here, and $5000 for related travel.

62. Page 39, Function 2528 Risk Management: Why are we increasing this requirement by $1.9 mil?

This is for Fund 299 Insurance Reserve. The requirement is based on the carry-forward balance from FY25-26. This fund is for possible future expenditures for insurance claims. Previously, this was budgeted in 2544 Maintenance Services and was moved to more accurately reflect the nature of future spending.

63. Page 39, Function 2529 Other Fiscal Services: Why are we increasing this requirement by nearly $800K?

This is the function for the set-aside from all grants that can be used to offset district costs to manage the grant (“indirect”). This is not an actual increase of $800,000, but the result of consolidating to one function. This amount matches the expected indirect allocation (4.14%) for grants eligible for indirect charges and shows as revenue to the general fund in object 1980, or 1000 Local Resources.

64. Page 40, Function 2544 Maintenance Services, 500 Capital Outlay: Why are we increasing this line by $5.6 mil?

This function reflects the cost for completion of the dental program classroom as well as the budget offset for Energy Efficient Schools. Note that 2544 is typically in Fund 100 as few grants pay for maintenance or repair expenses. However, Energy Efficient Schools requires a function/object for budgeting expenses and this grant only allows for capital expenses (e.g. equipment replacement). Typically, capital expenditures are budgeted and paid for through Fund 400 Capital Projects, and using the 4000 Facilities Acquisition and Construction functions.

65. Page 43, Function 3000 Total Enterprise and Community Service: FTE are staying largely the same but costs are increasing by $1.1 mil. Where and for what are costs increasing?

Nutrition Services (Fund 297) is most of the budget in 3000. The budget allows for negotiated classified salary increases (2% COLA, 4% Step, related payroll costs) as well as food cost increases.

Additionally, several grants have expenses charged here. For example, Title I uses function 3390 for parent and family events and Fund 242 for 21st Century Community Learning Centers to pay for SUN and other afterschool programs.

Fund 400

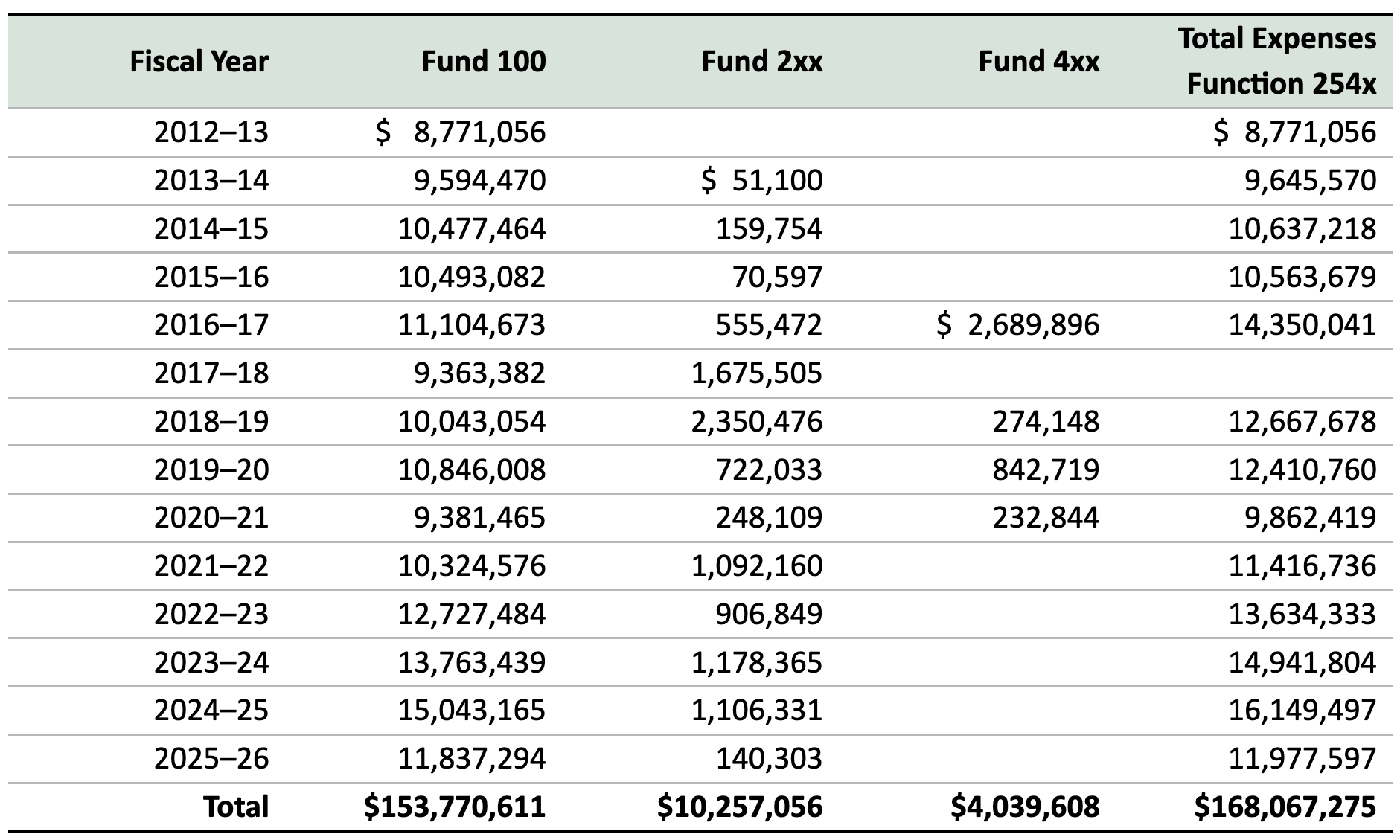

66. The Board's 2nd priority per our budget orientation packet is "Safe & Well Maintained Facilities" however the amount of budgeted expenditures in fund 400 has declined significantly from FY25-26 and there is no amount budgeted for objects 800 or 900 in FY26-27 which leads me to believe that we will deplete all fund balance in fund 400 during FY26-27. Can you give us more information about this decline in investment in capital projects while "Safe & Well Maintained Facilities" remains a Board Goal?

Fund 400 is funded by three mechanisms: A transfer from the general fund, receipt of Construction Excise Taxes, or a capital bond. The district has no open bond projects which is the decline noticed - as bond funds were expended, the Capital Fund declined. The general fund transfers sufficient funds for debt payments (Full Faith and Credit debt). New revenue from the Construction Excise Tax is also recorded to Fund 400, and carry forward funds are paying for the cooling tower project at RHS. Fund 100 is the primary source of funds to support facilities, which is limited when resources are stretched and classroom instruction is prioritized. When there is not a Capital Bond, expenditures are typically recorded in the Facilities, Maintenance, and Operations functions (254x). Below is a summary of the last 14 years of expenditures captured by 254x functions. Note that the 2xx (grants/special revenue) are predominantly from a state seismic upgrades grant prior to 2020 and COVID/ESSER funds from 2020 through 2025. Intensive Coaching funds have supplemented CTE program additions and we are just starting to see use of the Portland Climate Change project funds.

General Questions

67. Is outdoor school included in the budget?

In 2017, Oregon State University Extension Service (OSU Extension) was given responsibility for distributing funds to school districts and education service districts (ESDs) to establish and operate outdoor school programs. Every Oregon public school student has the opportunity to benefit from a hands-on, science-based outdoor education in fifth or sixth grade. https://extension.oregonstate.edu/outdoor-school/about-us. In the fall after outdoor school, the district is reimbursed for up to all costs, but the specific amount is not known until all outdoor school programs have concluded and OSU and MESD have reconciled available funds to reimbursement requests.

The budget includes State Revenue in the amount of $100,000 for this reimbursement in Special Revenue Funds

68. Doesn’t JROTC pay for itself?

Federal reimbursement is $45,255. The cost of the position assigned to ROTC is $159,058 (before changes for FY26-27 budget). Net cost for staffing is $116,803.

69. We adopted a balanced budget last spring but then found out there was a deficit in the fall. Can you explain this?

The budget was adopted with the inclusion of 10 furlough days. This was noted in the Revenue section in the line item “revenue hold” of $5,681,943. To enable budget authority for the possibility of furlough days to be added back during the year (if additional revenue had been received), the full cost of salaries without furlough was shown in expenses. The revenue hold of $5,681,943 represented the value of 10 furlough days or equivalent reductions.

70. Is board action required to approve the ending fund balance being below 5%?

The Board will need to take action on suspending “DBDB: Fund Balance” before the end of the fiscal year. This will be brought forward during the June Business Meeting.

71. Are we tracking how much we are losing from Measures 5 and 50?

It is difficult to say. This is a level of fiscal detail and research that is beyond the scope of our district’s financial team. Note since 1990, Measure 5 capped the amount that could be assessed “tax rate” on property values for public school funding. For this reason, it is difficult to determine what tax would have been charged without the cap. Measure 50 followed in 1997 to limit the annual growth of assessed value of property, which further reduced public school funding from local taxes. However, the State School Fund payment is reduced by the total amount of local revenue, such as property taxes. So, even with additional local taxes, those additional taxes would reduce the amount from the state payment - making the district’s resources neutral.

72. What level does the Budget Committee approve at?

The budget committee approves at the expenditure function levels (1000, 2000, 3000, 4000).

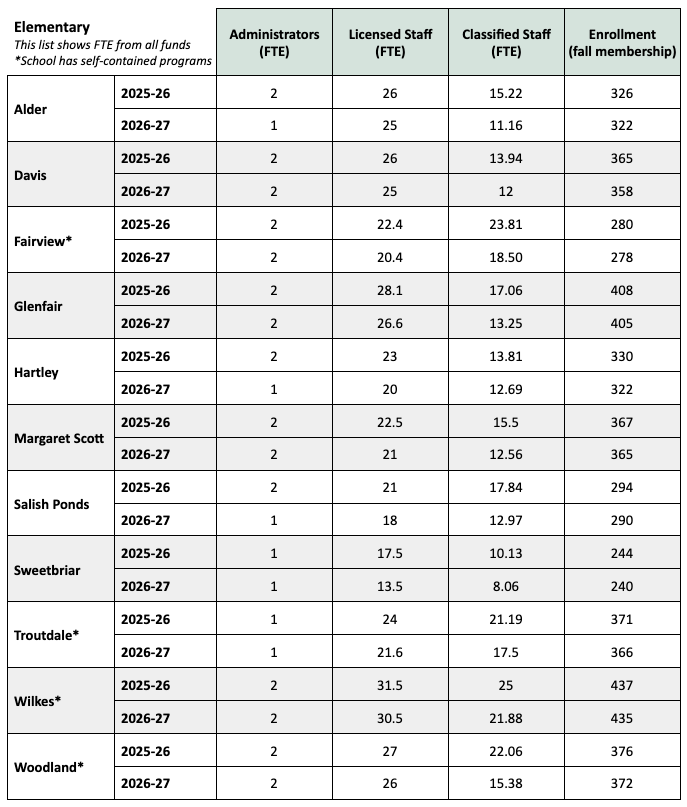

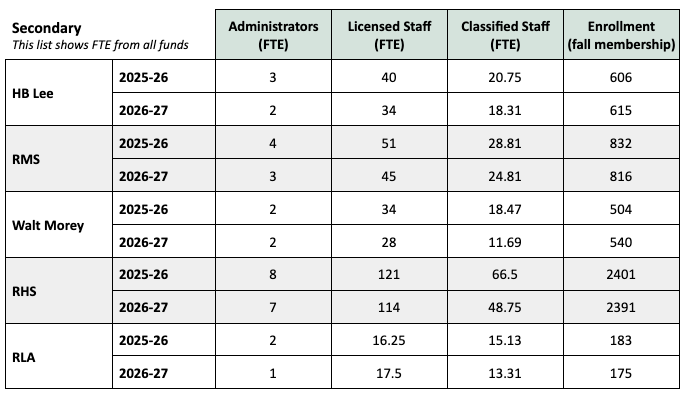

73. Can we get a list of changes in certified, classified, and administrative staff in each school, along with the enrollment numbers for this year and projected for next?

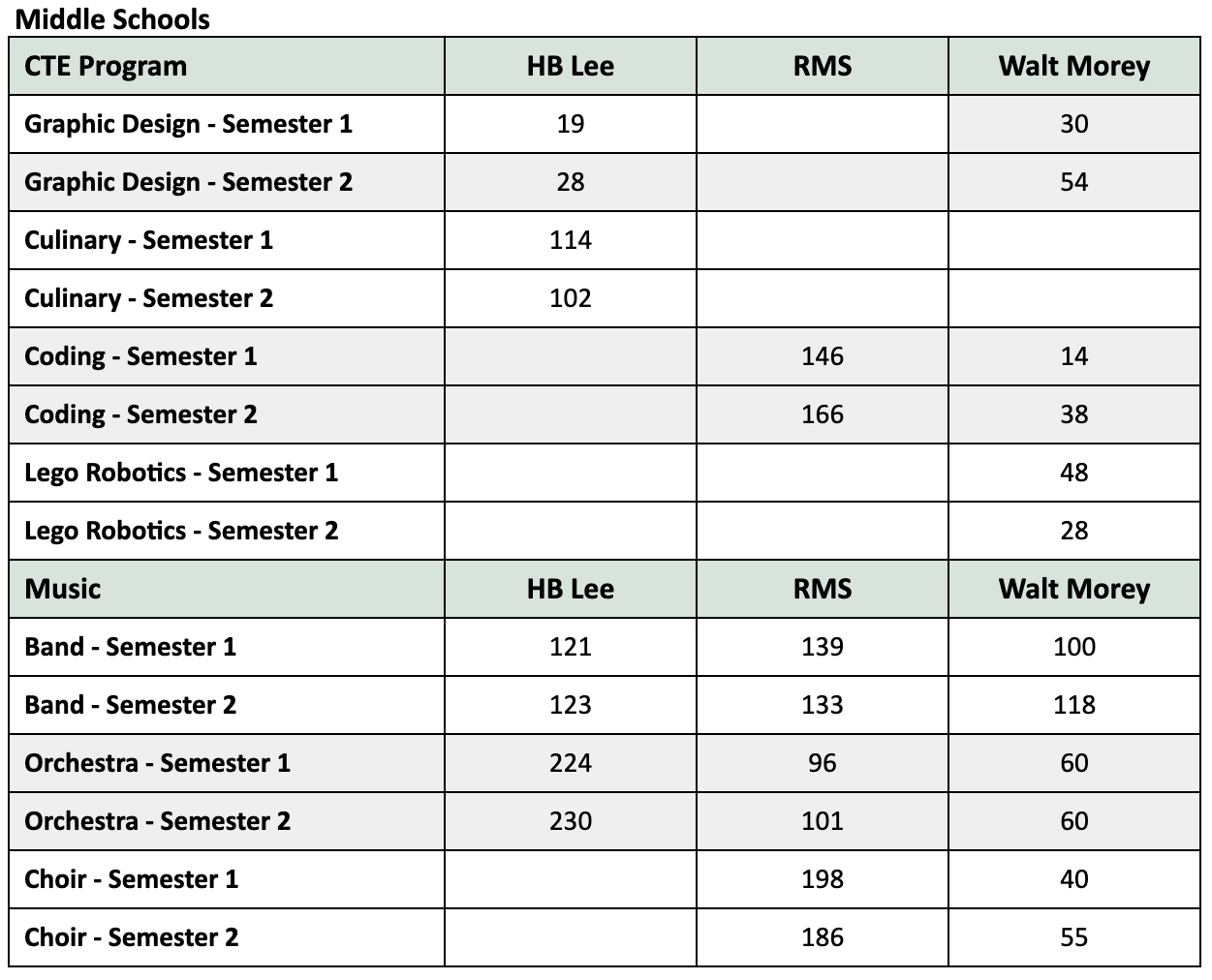

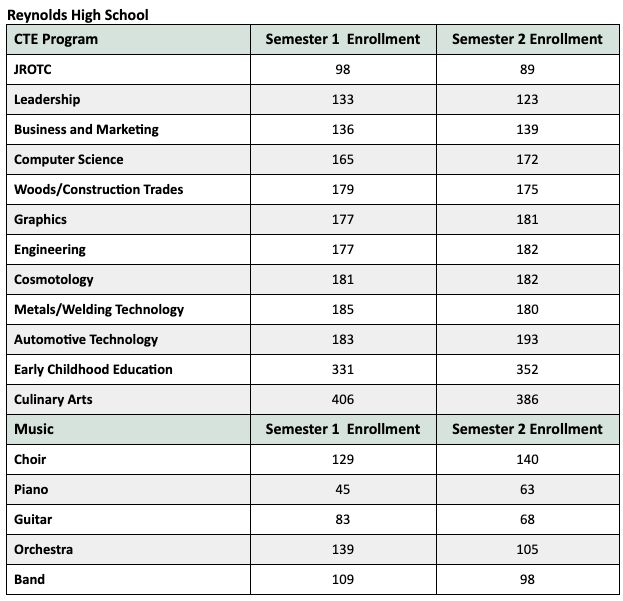

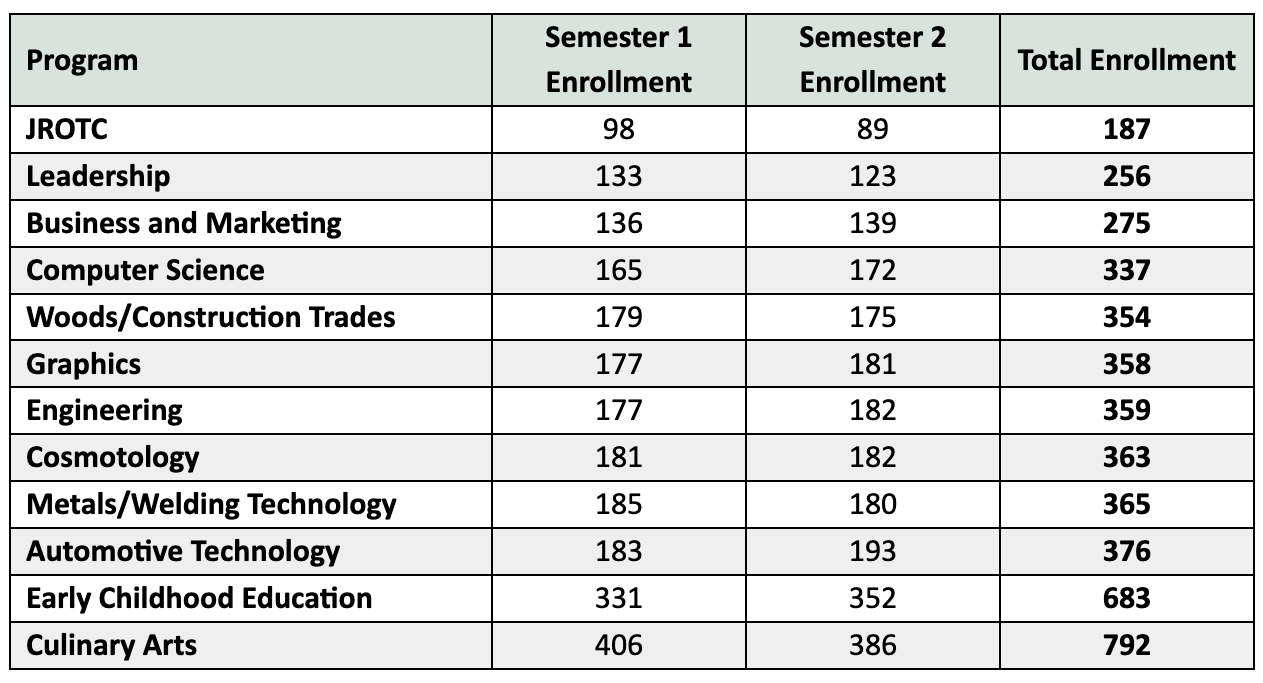

74. Can we get the number of students enrolled in music and CTE programs at the middle and high school level?

All numbers below are for the 2025-26 school year.

75. How much do cell phone stipends for admin cost? What about for all groups?

Administrators: $38,520

Specialists/Supervisors: $13,380

Licensed: $2,950

Classified: $23,750

Total Budgeted: $85,465

76. What does “salary regular” entail? What is included in “associated payroll costs?”

0100 Salary Regular” is all taxable compensation:

- 0111 Licensed Salaries (FTE)

- 0112 Classified Salaries (FTE)

- 0113 Administrator Salaries (FTE)

- 0114 Professional/Specialist/Supervisor Salaries (FTE)

- 0116 Supplemental Retirement Stipend

- 012x Temporary or Internal Substitutes (Timesheets)

- 0131 Additional Hours Licensed (Timesheet)

- 0132 Additional Hours Classified (Timesheet)

- 0141 Other Compensation Licensed (Stipends)

- 0142 Other Compensation Classified (Stipends)

- 0143 Other Compensation Admin (Stipends)

- 0144 Longevity Pay

- 0146 Travel Allowance (in lieu of in-district mileage)

- 0147 Cell Phone Stipend

- 0148 Stipend Bilingual

- 0152 Tax Sheltered Annuity

- 0164 SPED Staff 8% Stipend

0200 are the payroll taxes, insurance, and other contracted benefits:

- 0200 Fixed Costs (Typically used for vacant positions)

- 0210 PERS Costs

- 0220 Social Security

- 0230 Paid Leave Oregon

- 0231 Workers Compensation

- 0232 Unemployment

- 0240 Insurance

- 0241 Life and LTD

- 0242 EAP

- 0243 Insurance Pool

- 0245 Retiree Paid Insurance

- 0246 Tuition Reimbursement - Licensed

- 0247 Tuition Reimbursement - Classified

- 0248 Tuition Reimbursement - Administrative

- 0249 Administrator Professional Development

- 0250 Employee Assistance Program

Questions from the Public

View a PDF of the questions and answers

1. Why are charter schools continuing to take funds from neighborhood public schools? How much reduction in funds will they see?

Public charter schools in Oregon are governed by ORS Chapter 338, which outlines the formation, operation, and accountability of these independent public schools. The District has sponsorship agreements with four charter schools and the payment from the State School Fund is mandated through those agreements; the district cannot change the amount. The amount passed through to the charter school for 2026-27 is estimated to be $16,657,947.

2. With the proposed cuts to campus security, how do you plan to make sure that kids remain safe; especially at the high school level where my daughter constantly reports that there are fights happening in the halls?

Campus monitors at RHS are not being reduced.

3. With your proposed cuts to both the Special Education supports I assume that the population of students with behavioral/mental health concerns would be affected as well; what is going to be implemented to ensure that these populations don't fall through the cracks and get left behind?

The district will continue to partner with Multnomah County Mental and Behavioral Health services, the School Based Health Center at Reynolds High School, and SUN providers to refer students to care providers. In addition all schools will be staffed with full-time school counselors.

4. Please break down the reasons we are in a $21 million deficit for 2026-2027, after already having been in a $25 million deficit for 2025-2026.

When we provide the initial estimate for the budget, it is based on “rolling” all expenses forward - keeping the same level of services and staffing, or “Current Service Level.” However, maintaining the same level costs more due to inflation and cost of living adjustments.

Staffing costs increase every year when the district provides the step and COLA adjustments - meaning those same staff (FTE) cost more than the prior year. For example, if a step is 4% and the COLA is 2%, the same staffing level costs at least 6% more in salary, plus the increase to related payroll taxes. Similarly, our purchased services and supplies increase even if we purchase the same hours or items because costs increase for our vendors.

Our debt payments typically increase each year until the final year.

State mandates, such as changes to eligibility for unemployment in the summer and Paid Leave Oregon are adding to our costs. While these programs provide essential support to staff, these are additional costs to the district.

Insurance requirement changes have increased the cost to the district, such as increased costs related to workers compensation, sexual abuse, and cybersecurity insurance. The district is part of a state-wide pool. We have a limited amount of control over these costs.

PERS costs are increasing due to the state estimates of future payout of benefits. When so many districts increased staffing over the last five years, this impacted the actuarial calculation for future member benefits. Meaning, the more staff working now - the more benefits paid in the future. We are required to fully fund our PERS benefit, so as the future value of benefits increases, our current rates increase. PERS accounts for more than 30 cents for every dollar expended on compensation.

Note that while our staffing level and other costs have increased every year, our funding is based on student enrollment, which is declining. Since 2014-15 our student enrollment has dropped by 21% while our staffing has increased by the same amount. At the same time, the gap in our funding specific for special education relative to the cost of services is increasing while the number of students eligible for such services is increasing relative to the overall enrollment. So, our revenue driver is going down at the same rate as our expense drivers are going up. This results in a structural deficit.

The structural deficit has been increasing yearly over the past decade, but the ESSER/COVID funds helped delay the impact of this deficit as regularly occurring operational funds were moved to grant funds and left a greater ending fund balance to carry forward than before these funds were available. With these costs moved back to the general fund, we are now experiencing the full impact of cost increases beyond our revenue sources.

Specific to the differences from the current year to next year include:

- Meeting employee agreement requirements: Employee agreements require provision of step and COLA amounts, along with other items like stipends, insurance contributions, additional pay, tuition reimbursement, substitute coverage, and other working conditions with a cost impact.

- Return to a full school year: Furlough reductions to salaries saved approximately $2,718,052 plus related payroll taxes, which will be added back in FY27

- Less ending fund balance to carry forward: The district estimates a reduction of up to $6 million in revenue due to less beginning fund balance (which is the remaining funds from the prior year)

- Accounting for 5% Ending Fund Balance Requirement: Current service level expenses do not allow for meeting the board policy for retaining at least 5% of adopted revenues as the ending fund balance; we will expend about $4 million more than budgeted. To restore the ending fund balance, we either need to reduce expenditures or increase revenue.

5. How many administrators have been cut (in FTE)?

9.2 FTE (Administrators, Supervisors, and Managing Officer) were cut. 0.5 FTE was added to the General Fund for the Director of Federal and State Grants position, making the net reduction to General Fund 8.7 FTE.

6. How were individual student programs selected to be cut (e.g. JROTC)?

The decision to discontinue JROTC was made based on student enrollment and projected interest.

7. Why are student-facing staff being cut before non-student-facing staff?

Both types of positions are being reduced. There are fewer non-student facing positions to reduce as many were eliminated or reduced over the past several years. The majority of positions in a school district are student facing.

8. Why did Reynolds School District not use Oregon's SB 849 funds from 2025 for PERS relief? How can the district guarantee to its staff that if it receives dollars from the state that these dollars are used on our students?

The district’s PERS rates are inclusive of the 1.68% rate reduction applied through SB 849, which expires with this biennium (June 2027). The district is required to use funding as outlined by Oregon Department of Education, and spending is audited annually through a financial audit and through ODE desk audits (program reporting and reviews).

9. Why are temporary grant funds being used to make permanent changes to Reynolds High School's building, staff, and programming (i.e. the dental program)?

The Intensive Coaching Program funds are being used to fund the renovations necessary to establish a dental assisting program. High-interest programs at RHS are needed to engage students in pathways to living-wage jobs and future career opportunities.

10. Will we be cutting our contract with the Center for Advanced Learning (CAL)'s dental program?

For 2026-27, RHS students will be able to access three areas of study at CAL that are not presently offered at RHS: Nursing, Media, and Fabric Design.

11. Can we expect to have the same amount of reductions again next year? At what point does the district determine it has insufficient resources to operate?

Student enrollment is the main factor in the State Schools Fund allocation that Reynolds receives. For 2027-28 the amount of SSF will be determined by the Oregon Legislature at next year’s long session.

12. I am wondering what the thought process was in keeping AP positions while teachers are facing teaching blended classes next year with 30 or more students?

Assistant principal positions were reduced by 7 FTE–one each at RHS, RMS, RLA, and HB Lee, Hartley, Alder, and Salish Ponds. The elementary schools in which an AP was discontinued are projected to have enrollments at/under 350 and do not host specialized special education programs. Facing a deficit of this magnitude required balancing difficult choices throughout the organization.

13. What will the reduction to PE and music at the elementary level look like?

PE and music will continue to be offered at all elementary schools. PE and music staff will be shared between smaller schools. Larger elementary schools will continue to be staffed with full-time specialists. Additionally, Glenfair and Wilkes will have full time art teachers. Alder and Margaret Scott will share an art teacher. The art teacher positions (3 FTE) are funded through Portland Arts Tax. Schools that share PE and music staff will develop schedules to alternate days or weeks at each school.

Sample weekly time allocations based on the number of specialists available at each school confirm that adequate staffing will be available to cover contracted prep time: Sample Schedules

14. Why are we cutting counselors from elementary schools?

There will still be a full-time counselor staffed at every elementary school. One FTE was cut. It was shared between two schools as an additional .5 at each school. Facing a deficit of this magnitude required balancing difficult choices throughout the organization.

15. Are we cutting music or theater for middle school or high school?

No.

16. Why are OSEA and RAA getting COLAs this year? Why didn’t you cut benefits from the admin contract?

In 2026-27 OSEA and RAA both will be in the third year of their three-year agreement which includes a 2% COLA. REA opted for a two-year agreement which ends on June 30th, 2026. The budget includes the negotiated pay and benefits negotiated in the OSEA and RAA agreements.

17. Is Cabinet getting a COLA or steps?

The COLA increase stipulated in the Superintendent’s contract matches whatever COLA is received by REA, so 0% for 26-27. The Superintendent voluntarily will reduce pay by scheduled 3% step (the equivalent of seven days). The Assistant Superintendent and Managing Officers for Human Resources, Finance, and Operations do not receive steps and were scheduled to receive a 3% COLA. The full time positions will voluntarily reduce pay by that 3% (the equivalent of seven days). The Managing Operations Officer is reducing by .2 FTE.

JROTC Questions

18. Given that the program is heavily subsidized by federal dollars, all the ways that students benefit from this program, and its increasing popularity, why has the program been cut from the high school?

Total federal reimbursement is $45,255 for salary and related benefits. The cost of the FTE assigned to ROTC is $159,058 (before changes for FY27 budget) leaving a net cost of $116,803 to the general fund.

19. How much does this program cost the school district? What are the actual dollar savings from this elimination?

Federal reimbursement is $45,255 for salary and related benefits. Cost of the position assigned to ROTC is $159,058 (before changes for FY27 budget) leaving a net cost of $116,803 to the general fund.

20. Aren't we in the process of expanding our CTE program at the high school? JROTC is actually a CTE pathway in some states. Why are we cutting an inexpensive and growing program that fits within the CTE framework?

The program has a cost, like all others. Student interest in JROTC has decreased year over year and it is currently the lowest enrolled CTE program.

Superintendent's Budget Message

Dear RSD Community,

The 2025-26 school year has brought challenges and successes to the Reynolds School District. I want to thank all staff for their dedication to serving the students and families of Reynolds. As we look to the next school year, we continue to be faced with enormous challenges driven by a decade of decreasing enrollment, increasing costs, and an uncertain revenue outlook.

The statewide landscape that has shaped this budget includes falling state school funding due to a drop in enrollment, the cost of labor agreements, and the impacts of inflation. Unfortunately, state revenue for education was not increased during the February legislative session and is not sufficient for Reynolds to continue operating at the current program and staffing levels. In total, we are facing a reduction of approximately $20 million, or approximately 12% of the general fund, over the current service level.

Over the past decade our enrollment has dropped by approximately 2300 students, or 21%. This is part of a regional and statewide trend. While this year’s enrollment is slightly below projections, the ten-year trend is undeniable. Lower birth rates, the impacts of ICE activity, and unaffordable housing are significant factors. Enrollment is the main factor in the state revenue formula for funding schools, and when enrollment drops so does funding.

In planning the 2026-27 budget, we once again reduced central office and department budgets and staff and were required to make additional reductions including position reductions across all labor groups.

For the current school year, we had six furlough days and additional wage and benefit concessions from our labor groups in order to save the district approximately $5 million. I once again want to thank our staff for agreeing to furlough days which prevented approximately 50-70 more positions from being cut mid year. This budget assumes a full school year for 2026-27.

Last year at this time, I mentioned the report prepared by the American Institute of Research (AIR) at the request of the Oregon Legislature on Oregon’s school funding model. The report states that for districts such as Reynolds, the current model of state funding is inadequate to attain the achievement goals set by the state. The AIR report calculated that an additional $8,000 per student per year is required for the most highly impacted districts to reach the state goals. For perspective, in RSD that would amount to an additional $72 million per year, or almost an 80% increase in funding. Clearly what we receive from the state is insufficient to provide for all that our students need. Since then, there has been additional information on how the state’s calculation of student poverty shortchanges its most needy districts by millions annually, further validating the findings of the AIR report.

The 2026-27 budget is built on the following financial assumptions:

-

Projected September 2026 enrollment of 8,290 (non-charter)

-

State School Fund of $11.36 Billion for the 25-27 biennium, with a 49% / 51% split

-

Stable federal and state grant funds

-

Stable PERS rates for the second year of the biennium

-

An ending fund balance of 5%

-

Step, benefits, and cost of living increases for classified and administrative employee groups who enter the third year of their negotiated contracts.

It is our intention to align resources to the priorities of the district’s Strategic Plan, the Board’s budget priorities, and community input as a part of implementing the Student Investment Account (SIA). This will be the fourth budget I’ve presented and the third to include massive reductions. Our system is already at the breaking point, with all staff managing larger workloads with less support, and yet we will have to continue to reduce our staffing and programs in order to balance the budget. Every school and department will be impacted by the reductions we must make.

At the elementary level, under this budget every school will be impacted by larger class sizes and more blended classrooms, but our class sizes will remain in line with neighboring districts. Three smaller elementary schools will lose the support of an assistant principal. Each elementary school will maintain music, PE, library/media specials, but smaller schools will share music, PE, and reading specialists between two schools. A full time library/media specialist and counselor will continue to be staffed at all elementary schools. Elementary schools will also have one full-day, full-year educational assistant funded through the Early Literacy Grant to support kindergarten literacy instruction and student transitions.

We will continue important programs but at a pared down level. Block schedules at the middle schools will remain, although with significant reductions to staffing levels. The effectiveness of the block schedules at the middle level continues to meet student needs. Reductions at the middle level will increase class sizes, but again are in line with neighboring districts. Unfortunately, at current funding levels, we will be required to pare down our middle school sports program by discontinuing wrestling and cross-country. Each school will still have volleyball, basketball, and track and field teams. We will continue to partner with SUN and PlayEast to provide a robust and low/no cost slate of student activities including opportunities for sports for middle school aged students.

At our high schools, the reductions will be felt in larger class sizes, less electives, and fewer student supports. At RHS, the Senior Inquiry and JROTC programs will be discontinued. Students will continue to have a robust selection of college credit earning classes through the AP and dual-credit programs, as well as 11 CTE programs including a new program training students for careers in dental assisting. Additional reductions include reduced attendance, counseling, and office clerical supports, and reduced seats for middle college, the Center for Advanced Learning, and for alternative private high school placements. RLA will also have larger class sizes and fewer options.

Over the past three years, we have largely been able to avoid significant reductions in special education staffing. Unfortunately that is no longer an option. Due to underfunding from the state to serve students with disabilities, we continue to tap into the General Fund to fill the gap. Reductions in special education staff will increase caseloads and workloads, but will remain comparable with neighboring districts. Staffing reductions will increase caseloads for speech/language pathologists, school psychologists, and resource teachers. Additionally Teacher on Special Assignment positions will be reduced.

English language development (ELD) programs will not be reduced. This year, ELD instruction at the elementary level underwent a shift in service delivery necessitated by previous staffing reductions as well as to improve instructional efficacy. The shift in the elementary delivery model to an integrated language block is underway at all schools and initial indications are that while there are always challenges in implementing something new we are seeing improvement in student outcomes.

In this budget, there is an additional $3.5 million in reductions in central office and support services. The reductions include administrative, licensed, and classified positions and contracted services in Custodial, Facilities, Transportation, Curriculum and Instruction, Human Resources, Operations, Language Services, Finance, and Information Technology.

We will continue to partner with Multnomah County for additional support for students and families through investments in the SUN Community Schools program and our School Resource Officers. Multnomah County also provides us services at no additional cost to staff the Student Health Center at Reynolds High School, as well as school based mental health providers at multiple schools.

This is challenging news for all of us, and I continue to be heartbroken by the lack of funding for our schools. However, it is our responsibility to present a balanced budget that lives within our means as a district.

The proposed budget leverages state and federal grants to support our students primarily through funding staff positions. In total this budget will support 263 positions ( 225.22 FTE) from grant funds. While the large majority of these grant funds are considered stable, 16.5 FTE are funded through limited duration grants and will require future budgetary choices when the funding runs out. Additionally the actions of the Federal government continue to give us cause for concern about the future of Federal funding streams. We will continue to monitor Federal actions on education closely.

I will continue to advocate for a state school budget that better meets the needs of Reynolds. Our advocacy is focused on three core areas in the state budget that would have a significant impact:

-

Increase or remove the special education cap from the current 11%. Students with disabilities make up 18% of Reynolds enrollment, and the state funding formula only provides reimbursement for 11%. This equates to upwards of $6 million dollars of underfunded costs for Reynolds, and less so every year that overall enrollment decreases.

-

Increase the reimbursement for high-cost disability expenses. Our high-cost disability costs are annually over $5 million, and last year we were reimbursed at approximately 21%. This also equates to millions of dollars of underfunded costs for RSD.

-

Reform how ODE allocates funding for students experiencing poverty. ODE’s current funding model drastically undercounts how many students in RSD are navigating poverty, resulting in additional underfunding of approximately $7 million dollars annually.

In closing, I want to thank the School Board, educators, support staff, administrators, and the Reynolds community for their dedication to students. I want to recognize the hard work of our Finance and HR teams in preparing the proposed 2026-27 budget. We’ll continue to move forward and meet the challenges of educating our children in these uncertain times. We’ll continue to advocate at the state level for not only our students but all Oregon students. We’ll continue to look for ways to innovate and improve. And we’ll continue to partner with our community to ensure that all students succeed.

Thank you for your consideration of the 2026-27 Proposed Budget.

Frank Caropelo

Superintendent

Budget Development

This list is preliminary. It reflects the district’s current and projected financial information, projected 2026-27 state revenues, negotiated wage, and benefit increases for OSEA and RAA in year 3 of their contracts. It reflects the district’s proposals for wages and benefits for REA.

Impacted Groups |

Approx FTE

|

|

|

Elementary Schools |

Class Ratio Adjustment (1:28) Reduced or Discontinued:

|

- 51 |

|

Middle Schools |

Class Ratio Adjustment (1:34) Reduced or Discontinued:

|

- 31 |

|

High Schools |

Class Ratio Adjustment (1:34) Reduced or Discontinued:

|

- 24 |

|

K-12 Supports |

Reduced or Discontinued:

|

- 12 |

|

Centralized Services |

Reduced or Discontinued:

|

- 14 |

|

Special Education |

Reduced or Discontinued:

|

- 26 |

Total Estimated Savings: $17,600,000 |

Total FTE: - 158 |

|

Budget FAQs

Would moving to a four-day school week save the district any money?

In considering a four day week, there are financial and academic impacts, as well as impacts on families to consider.

Academic Impacts:

- Here’s a report from the University of Oregon on four-day weeks. Beyond this, the research consensus is that students who are in four-day week schools in non-rural areas achieve less, earn less credits in high school, and have a lower graduation rate than their peers who attend five-day week schools. It also has a negative impact on students with disabilities and English learners as they receive less exposure to instruction and have greater gaps between instruction.

Impact on Instructional Time:

-

Additionally, to meet instructional minutes using a four-day week, we would have to increase instructional time on the other four days.

- If we shifted to four full days, to get the same number of minutes, we would have to increase each day by 70 instructional minutes. This would make for a long student day, as well as push the teachers’ day to be even longer. Alternatively, to keep the student day at a more reasonable length, some districts bundle teachers’ prep time and put it all to the fifth (non-student) day per week. This is also when staff meetings, PLC meetings, and IEP meetings are held since the student contract days become very long and after/before school meetings are not productive or desired. Since the schools remain open five days, there’s no savings on utilities, office, or admin staff.

Financial impact:

-

The financial impact of switching to a four-day week has been estimated to save approximately 2% of a district’s budget. For RSD that would amount to about $2.5 million per year. It definitely is a savings we could use, but at what expense?

- There is also the impact on classified staff to consider. On a four-day week, many student-facing classified staff—paraprofessionals, campus monitors, bus drivers, nutrition, etc, would not work on the non-student day. They would lose 20% of their hours each week. This is a huge burden to place on one group.

Impact on Families:

-

There would also be a significant impact on the families we serve as they would have to find childcare on the fifth day or rearrange work schedules. Many families also rely on school provided meals.

- The impact on families would certainly lead many families to request a transfer to our neighboring districts that remain on a five-day schedule. It would only take about 200 students leaving our district to wipe out the $2.5 million in savings. Ultimately shifting to a four-day week could leave us in a worse financial position.

While there are advantages to a four-day school week from a work/life balance perspective, the negative academic impacts and small financial savings (or possible loss) don’t seem to outweigh them.

Have you thought about closing a school?

At this point, closing a school would not be a huge financial savings. At the middle school level, no two of our buildings are large enough to absorb the students from a closed school. At the elementary level, closing a smaller school would overcrowd other schools, and the cost savings from closing an elementary school are relatively minimal as staff follow the students. We are not there yet, but might be in future years. We are expecting to receive updated demographic forecasts this spring that will help us to understand enrollment patterns for the next decade.

When a school is closed and students are relocated, staff are needed to support the students at the larger school, so not much is actually saved in closing a school—some utilities and a few support positions such as a principal and office staff.

We estimate less than $500-800K per year would be saved by closing an elementary school, which has to be weighed against the immediate impacts (losing students to private and charter schools, the costs of maintaining a “closed” building that may be needed in the future, increased busing costs, etc) and long-term demographic trends (will the building be needed in the future?, what else can we do to operate more efficiently?).

What is the timeline for notification regarding reductions in force?

We are in the process of determining the total dollar amount we need to reduce for next year's budget. After that, we will finalize the plan for overall reductions. Then, we review school enrollment projections to determine staffing levels. After that, HR meets with REA and OSEA to review seniority and any bumping/ transfers that must occur per the CBAs. Then we are able to inform individual staff members about the potential for reduction in force. We then must wait for the budget to be approved before moving ahead with any staffing changes. Reductions in force take effect on June 30th or the last workday of the school year.

If student-facing staff have been reduced/will be reduced, then it stands to reason that there is less staff for the district administration to support.

Unfortunately, there is very little that could be further scaled down due to staffing reductions from what’s already been reduced from central office administration over the past three years. Payroll, for example, still takes two FTE whether we employ 1500 or 1200 or 900 staff. Most all centralized management positions such as in transportation, operations, IT, C & I, HR, Finance, and Nutrition have been reduced over the past three years.

The current level of staffing is needed to accomplish the work that is required by the CBAs, insurance requirements, and state laws. There are 296 Reports that must be submitted to ODE annually. Every one of these reports requires staff time to prepare and submit. It is not simply hitting a button in the system. This is just one example of the many requirements to run a school district. Other areas of non-student facing support staff such as TOSAs were significantly reduced or completely eliminated three years ago.

Why are we adding electives (Dental, Cosmetology, etc)?

The start-up costs for new CTE programs like Cosmetology, Business, and Dental Assisting are funded through the Intensive Coaching grant, not general fund. This grant will be in its final year in 26-27 and cannot be renewed. The grant is intended to be used to improve district outcomes.

By creating new CTE programs, we hope to retain more students at RHS as well as improve graduation rates. These outcomes will benefit our students as well as our budget in the long-run. We chose to use some of these short-term funds for program development so that when the grant ends, the program infrastructure remains to serve our students for years to come.

As our recent financial audit showed, we do not have reserve funds or “found money” in the budget. We must either increase revenue or reduce expenses, or both. Revenue comes from enrollment which is why developing programs that attract and retain students such as CTE, dual credit, preschools, and dual language immersion are critical to keeping kids and families connected to our schools.

Purchased Services is the largest item in the budget, after salaries and benefits. Have you looked at reducing this area?

The table below shows a breakdown of what is actually in the “purchased services" expenditure category. Unfortunately, most of what falls in this category is required spending either by law or policy. The areas within purchased services that could be considered discretionary are things like the SUN and SRO contracts, Schoology, AVID, Mt Hood Middle College, PSU Senior Inquiry, textbooks, Graduation, etc. Many of these have and will continue to be scrutinized for savings.

Category |

24-25

|

25-26 Estimated |

Description |

|

Charter Schools |

$14,259,834 |

$18,328,523 |

Required by Contract |

|

Special Education Outside Placements |

$4,855,609 |

$5,204,034 |

Required by IEPs |

|

Substitutes (ESS) |

$3,253,719 |

$4,135,252 |

Required by Contract |

|

Utilities |

$3,809,898 |

$3,677,659 |

Electric, Water, Sewer, Garbage, Internet, Security |

|

Custodial Supplies, Equipment, Maintenance & Repair |

$2,903,414 |

$2,090,272 |

Does not include staff |

|

Required Services by Law or Policy |

$813,251 |

$1,114,840 |

Examples include: Financial Audit, Insurance, HR/Financial Services, Legal Services, Elections, etc |

|

Curriculum, Instruction, Technology, Student Programs |

$3,458,828 |

$2,366,651 |

Examples include: SUN, SRO, MHCC, Synergy, Schoology, Student Laptops, AVID, PCC, PSU, Copiers, Core Curriculum, HS Sports, Graduation, etc. |

Total |

$33,354,553 |

$36,917,232 |

|

Budget 101 Q&A Session - February 19, 2026

Here's the video from the Budget 101 session. You can see the questions asked and the answers below.

Questions and Answers:

What percentage of our payroll goes to PERS?

-

PERS is about 26% of salary costs, which is the cost to pay our PERS bond (12%) and to pay the PERS employer contribution (14%)

- A PERS obligation bond is a way to borrow money that has to be paid back with interest

- The district invests bond receipts and the earned interest is used to offset PERS costs

-

Our rates include a reduction for the PERS Bond savings that are applied to “buy down” our rate, as well as a state-wide reduction of 1.68% for just this biennium:

- Tier 1 / Tier 2 increased by 10.27% from 8.43% to 17.02%

- OPSRP increased by 9.93% from 5.59% to 13.84%

- PERS rates and explanations for the changes are on the PERS Website here

- PERS rates are set each biennium in odd years

There was a recent decision to stop having building subs - how much money were we able to save from that? And where can I find that in the budget?

It is unclear if discontinuing building based substitutes will be a cost savings. The amount saved depends on the number of substitutes that are needed to be called during the school year. Building based substitutes were not district employees, and their use did not replace an ESS substitute. It was simply a way to make sure schools had a ready substitute on hand who knew the school and students. When use of the building based substitutes dropped below 90% their use was discontinued.

Is RSD pursuing the State Summer School Grant? If so, is it for K-5 or K-8?

Yes. ODE just released the competitive grant application. Submissions are due by March 20. We likely won’t know the amount of the award until sometime in April. We are applying for K-12.

Is there an easy way to tell what categories items belong under in the budget? Where can I find a description of the functions and objects (what they mean and what is included in them)?

Budget categories are determined by ODE in the Program Budgeting and Accounting Manual (PBAM).

The budget and expenditures are grouped by three elements:

-

Fund

- 100 General Fund: Unrestricted costs are primarily budgeted in the General Fund, along with essential operating expenses

- 200 Grant/Special Revenue Funds: Generally supplement (not replace) the general fund; these are often restricted by the funder to specific purposes

- 300 Debt Funds: Restricted to managing our bond repayment

- 400 Capital Funds: are used to manage bond-funded projects and Construction Excise Tax projects; both are restricted to specific uses related to capital construction efforts

-

Function

- 1000 Instruction Services

- 2000 Support Services

- 3000 Community Services

- 4000 Facilities Acquisition and Construction

-

Object

- 100 - Salaries, stipends, additional hours, taxable compensation

- 200 - Taxes and benefits

- 300 - Services (charter school payments, utilities, property services and repairs, contractors, substitutes, etc)

- 400 - Supplies and equipment

- 500 - Property, buildings, technology, or equipment purchases exceeding $5,000 and lasting longer than one year

- 600 - Dues, fees, taxes, principal and interest payments

On the purple assumptions sheet, the “all other sources” resources category goes from an estimated $7.7m this year to $4.6m next year. Why is that expected to go down by $3m?

All Other Sources is the sum of General Fund revenue other than the State School Fund Formula revenue.

- Local sources - we believe we will have a reduction due to interest earning. As we spend down available cash balances we also reduce interest earning

- Intermediate sources - this is primarily the pass through funds we receive from Multnomah ESD, or what is called “transit” funds. Transit funds are the balance of funds available after we pay for special education services (outplacements) and regionally-shared technology and infrastructure. We had accrued a transit balance and pulled that as one time funds for this year ($3 million); $500,000 to $1million is typical.

- State Sources - this is our reimbursement for high cost disability expense, and the amount has been reduced each year due to the growing need across the state. We do not know what portion of our actual costs will be reimbursed until we actually receive the payment. The reduction reflects the overall trend in the last five years.

- Federal sources - this is the partial reimbursement we receive for our JROTC program, and in applicable years, FEMA disaster funds.

Does the grant money show up in the general fund?

No. General fund is fund 100. All grants are in Fund 200.

Why are you showing a 5% increase for health insurance but it’s capped at 4.5% by OEBB?

OEBB offers many plans across the state. They have a policy to cap average policy increases to 4.5% across all of the plans. The district offers only a selection of those plans; our specific selection within those plans may be more or less than the 4.5% average (e.g. Keizer Plan 1 could be a 10% increase, but Moda Plan 3 is a 2% increase - an average of 6%)

Schools are moving toward offering dual language programs. How much is this expense? Do we have a plan to offset?

Dual language programs have minimal additional startup expenses related to additional curriculum materials. Those costs have been covered by the Intensive Coaching grant. When new materials are purchased, materials for DLI will be part of the purchase and not additional. DLI classrooms are staffed as part of the school staffing plan, not with additional FTE.

Budget Meeting Information

April 2: Budget Committee Work Session / Training | Presentation

April 30: Budget Committee Meeting 1 (6:00p) | Agenda | Presentation

May 14: Budget Committee Meeting 2 (6:00p) | Agenda | Presentation

Budget Committee

According to Policy DBEA, "The district budget committee will consist of the seven members of the Board and seven electors appointed by the Board as required by law. The term of the appointed members of a budget committee in a district that prepares an annual budget, will each be three years, with appointments made so that, as nearly as practicable, the terms of one-third of the members end each year. At least one member of the budget committee must be a member of the district’s educational equity advisory committee. The Board will establish appropriate timelines and procedures for the appointment of budget committee members."

Budget Committee Members

Position 1: Aaron Muñoz (board member, term ends 6/30/29)

Position 2: Joyce Rosenau (board member, term ends 6/30/29)

Position 3: Michael Reyes (board member, term ends 6/30/29)

Position 5: Patty Carrera (board member, term ends 6/30/27)

Position 6: Ana Gonzalez Muñoz (board member, term ends 6/30/27)

Position 7: Francisco Ibarra (board member, term ends 6/30/27)

Position 8: Vacant (community member, term ends 6/30/26)

Position 9: William Ohle (community member, term ends 6/30/26)

Position 10: Vacant (community member, term ends 6/30/26)

Position 11: Victoria Rizzo (community member, term ends 6/30/27)

Position 12: Catherine Nicewood (community member, term ends 6/30/27)

Position 13: Vacant (community member, term ends 6/30/28)

Position 14: Margaret Breithaupt (community member, term ends 6/30/28)